Community

Sharath Kuruganty

Travis Stephens is Chief Revenue Officer at Agent and an active investor in private markets. Previously Chief Strategy Officer at 10 East, the Harvard Business School graduate has seen firsthand how the right tax strategy can optimize outcomes—and minimize wealth leakage.

Tax is the largest, and often most overlooked, expense in investing.

For decades, investors have devoted seemingly infinite resources to diligence, sourcing, and structuring…all in pursuit of a modest edge, quantified as a point or two of ‘excess return.’

In this relentless optimization of pre-tax performance, one critical dimension has been largely ignored: tax. This blind spot stems, in part, from a legacy industry mindset, one architected around non-taxable LPs. But private markets have evolved. And we are taxable…entrenched legacy bias is thus no longer relevant.

We’re entering an era where ‘tax-alpha’ will be front of mind, a renewed focus on minimizing tax drag, preserving wealth, and maximizing after-tax returns.

…

Meet Alex. He lives in San Francisco, loves chocolate cookies, podcasts, and long walks on the Embarcadero, ideally with a Philz coffee in hand. He's also an active investor.

What Alex doesn't love? Taxes. In fact, he used to avoid even thinking about them.

"Sure, taxes might be my biggest expense," he'd tell himself, "but not if I don't think about them…"

And so, like many bright technologists before him, Alex drifted into a comforting fog of cognitive dissonance.

What Most Investors Miss: Tax Moves That Cost Millions

Alex was early at Uber. When the stock finally ran, he exercised all his Incentive Stock Options (ISOs) at once—without modeling for the Alternative Minimum Tax (AMT).

Exercising 40,000 ISOs at a $1 strike when the fair market value hit $50—creating nearly $2 million in AMT income and a ~$540k tax bill on paper gains he couldn't even sell.

The AMT credits took years to recover, leaving him with trapped capital and a painful liquidity mismatch.

Flush from the Uber windfall, Alex bought a home. But with the SALT deduction capped at $10k, he didn't get much benefit. (Note: for 2025 returns, the Federal SALT cap is $40k with an income phase-out; earlier years were capped at $10k.)

The mortgage interest helped a little, but not enough to offset high-income years.

Later, Alex added a long-term rental to his portfolio but skipped a cost-segregation study, taking slow depreciation and paying more tax on other sources of passive income much sooner than he should have.

When he gave to charity, he used cash instead of donating appreciated stock, meaning he paid unnecessary capital gains.

To top it all off, he didn't realize he'd missed quarterly payments and had been accruing penalties.

Then came the next chapter: Alex left Uber to ride the AI wave and founded his own company.

The company took off, and the exit came in under five years. But he hadn't set things up to qualify for Qualified Small Business Stock (QSBS, §1202).

That meant he was fully exposed to federal capital gains tax, the Net Investment Income Tax (NIIT), and California tax (since CA doesn't conform to QSBS exclusions).

Alex worked hard. He even optimized for talent density. But despite all that effort, he ended up leaking a lot in taxes.

In summary, Alex left millions on the table.

The Tax Playbook: How To Preserve Your Upside

In a smarter version of this story, Alex teamed up with a tax advisor or a service like the one he’s using (Agent.tax) before exercising his stock.

He modeled AMT headroom and split up his ISO exercises across years when the fair market value was lower.

That dropped his AMT bill to ~$110k, and sped up his credit recovery.

His long walks became a lot more relaxing.

From day one of his startup, he documented QSBS eligibility early, using spousal and non-grantor trusts to multiply the $10 million federal exclusion per taxpayer. (Still paying California tax, of course.)

On the rental, he commissioned a cost-segregation study to front-load deductions and offset passive income.

For charitable giving, he bunched donations into a Donor-Advised Fund (DAF) and gave appreciated stock instead of cash, avoiding capital gains while getting fair-market-value deductions.

He stayed penalty-proof and flexible by hitting safe-harbor thresholds to minimize penalties.

He covered all the foundational tax basics: maxing out his 401(k), backdoor Roth, and HSA contributions; bunching charitable deductions; and deferring bonuses or income where possible.

The result? Alex preserved far more of his hard-earned wealth and was able to invest in more opportunities on Goodfin.

The Result: $1M+ in Tax Savings–and Peace of Mind

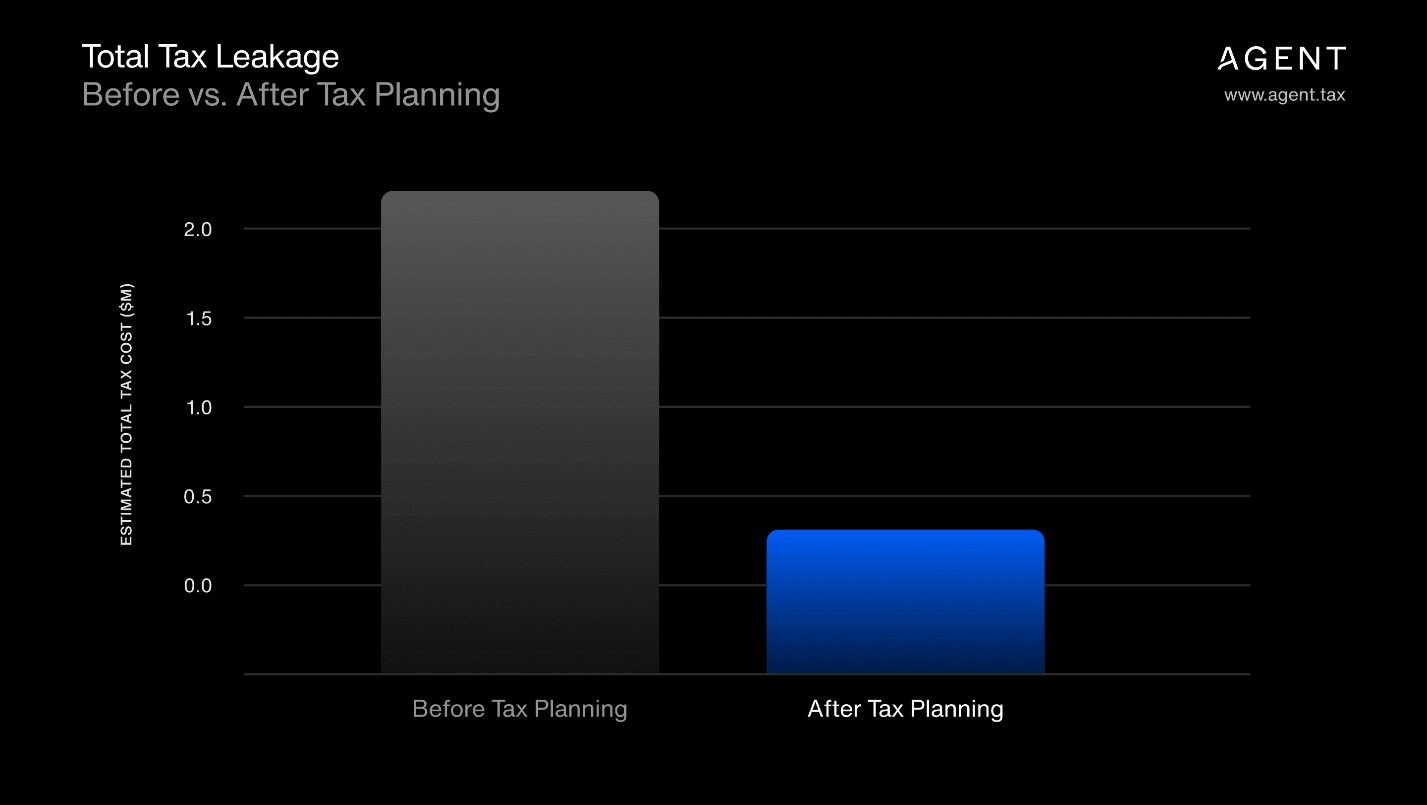

Before vs. After: Visualizing Tax Leakage and Planning for it

Smart tax planning transformed Alex's financial picture across every category.

For instance, by modeling his AMT exposure and spreading exercises, he reduced his AMT burden by ~65%.

Setting up QSBS eligibility cut his potential capital gains tax materially.

Strategic steps like cost segregation, donating appreciated stock, and avoiding penalties drove further efficiency.

Altogether, these adjustments freed up more than a million in liquidity that would have otherwise gone to taxes—capital that could instead compound and build wealth.

Peace of mind.

At Goodfin, smart investing starts with smarter insight. We're building an AI-first, high-trust home for GPs, operators, and allocators to share the tactics and tools that actually work. Join the conversation, explore member content, and start making your capital work harder—all inside Goodfin. → Join as a member

Read More